Our goal is for all Tanzanians to derive value from the regular use of financial services

Driving the financial inclusion agenda to overcome persistent exclusion among marginalised groups

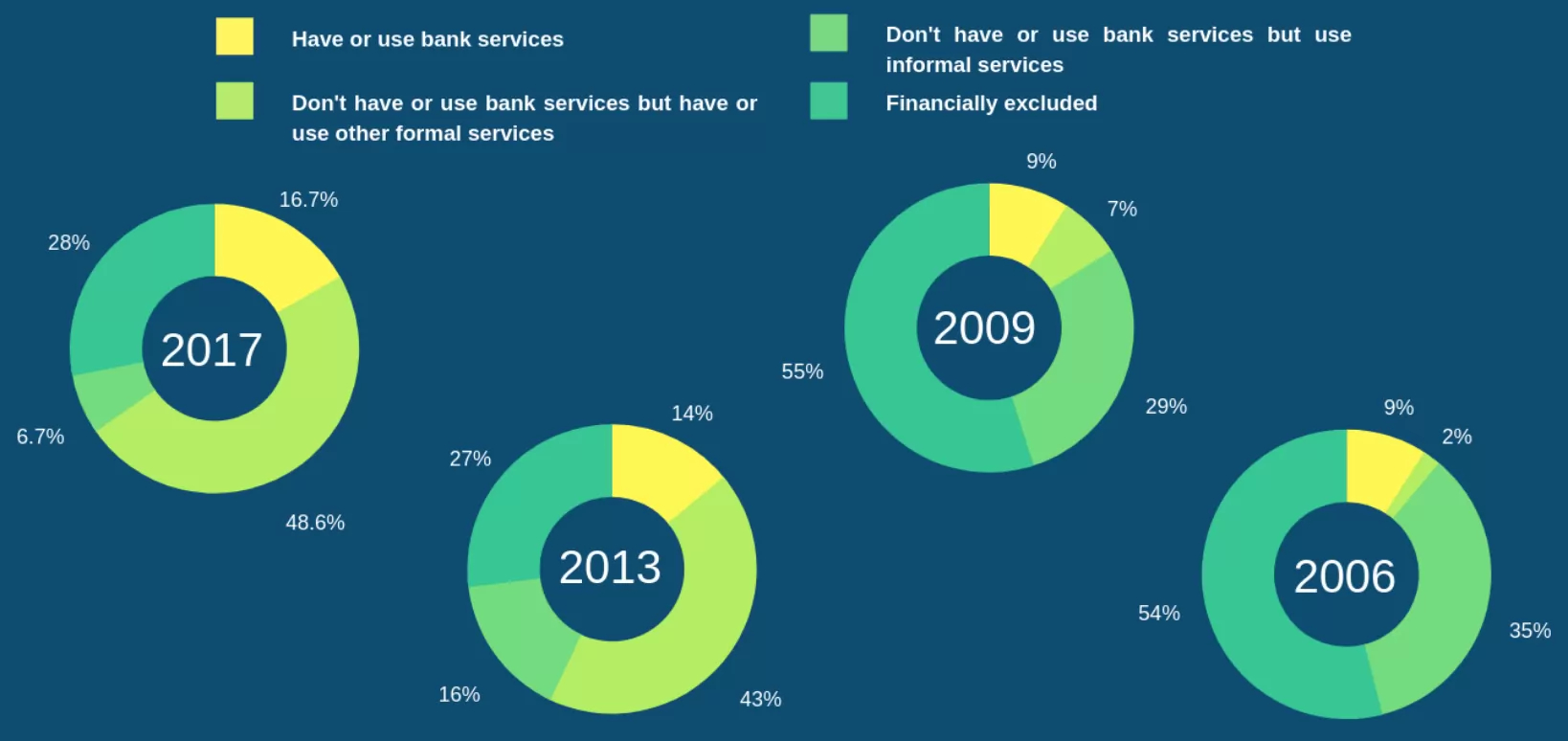

Great strides have been made in improving formal financial inclusion from 11% of the adult population in 2006 to 65% in 2017, attributed to innovative strategies among financial service providers and regulators, the rapid evolution of mobile solutions and the expansion of access points across the country.

11%

of the adult population in 2006 to 65% in 2017, attributed to innovative strategies among financial service providers and regulators

Challenges

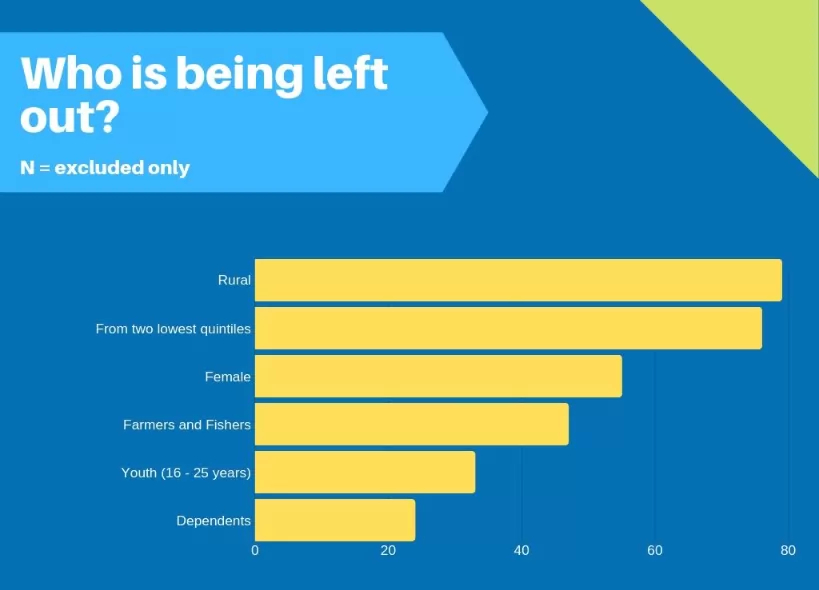

The results are promising, but evidence shows that there is more work to be done to reach key groups who remain financially excluded, namely women, youth, rural dwellers, farmers and small business enterprises.

of the adult population in 2006 to 65% in 2017, attributed to innovative strategies among financial service providers and regulators

61%

Only 61% of Tanzanian women are financially included

30%

unbanked are between the ages of 15 and 24

79%

of those who are financially excluded live in rural areas

10%

Only 10% of farmers use formal financial services

4%

of small businesses are formally registered

Our commitment to the groups we serve

The challenge going forward is to close the demand-supply gap among these groups through public-private partnerships, innovative policy and customer-led financial service provider strategies.

We work to overcome information asymmetry on the supply side which limits appropriate, customer driven innovation, as well as legislative barriers and rigid requirements for customer registration.

On the demand side, we collaborate across the sector to recognise the needs of marginalised groups to inform appropriate, cost-effective provision of financial products and services.